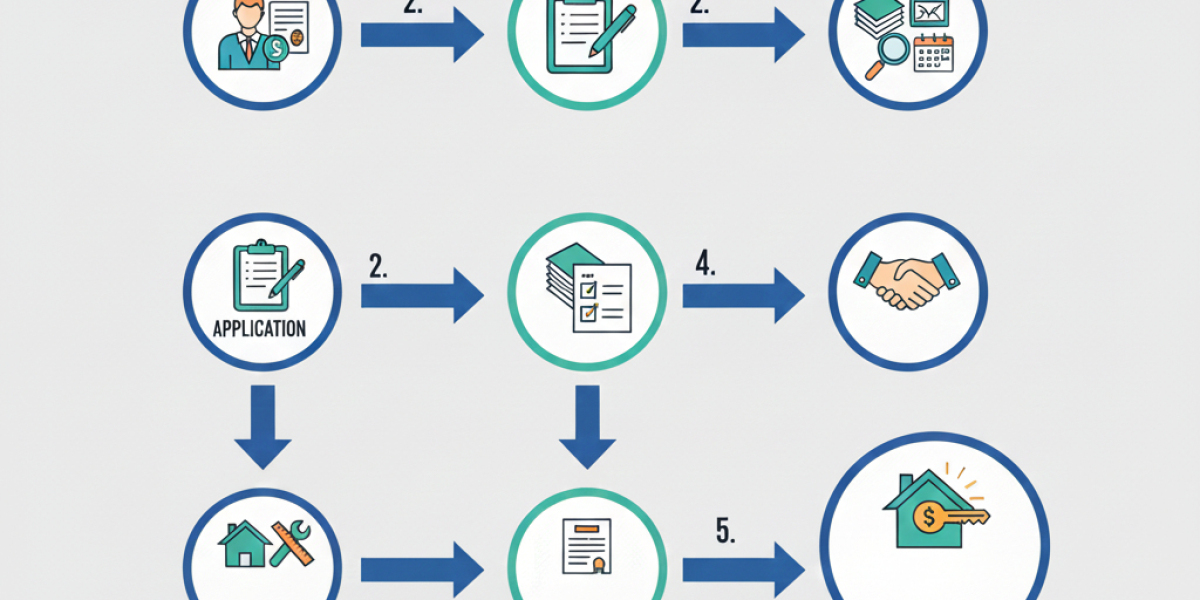

Introduction

Getting approved for a mortgage can feel like navigating a maze, especially for first-time buyers. While the jargon and paperwork may seem intimidating, the approval process is a series of logical steps designed to ensure you and the lender are a good match. Understanding each stage helps reduce surprises, speeds up approval, and increases your confidence as you move toward homeownership.

Pre-Application Preparation

Before you speak with lenders, get your financial house in order. Check your credit report and score, gather recent pay stubs, tax returns, bank statements, and records of other debts. Calculate your debt-to-income (DTI) ratio and decide how much you can comfortably afford for a down payment and monthly mortgage payments. Taking care of small credit issues, like paying down high-interest cards, can improve your approval odds and help you secure a better rate.

Getting Pre-Approved

A pre-approval is a lender’s conditional commitment based on an initial review of your finances. You’ll submit income documentation, authorize a credit check, and provide details about your assets and employment. The lender will estimate how much you can borrow and may issue a pre-approval letter you can show to sellers. This step strengthens your negotiating position because it signals that a lender has already vetted your financial situation to some degree.

House Hunting and Making an Offer

With a pre-approval in hand, you can shop for homes within your budget. When you find a property you like, make a purchase offer that may be contingent on mortgage approval and a satisfactory appraisal or inspection. Once the seller accepts, you’ll move from conditional steps into the formal mortgage application process—this is where things become more specific and binding.

Formal Mortgage Application

After your offer is accepted, you submit a full mortgage application. This includes completing the lender’s detailed forms and providing any documents requested during pre-approval plus potentially more recent pay stubs, updated bank statements, and clarifications on employment gaps or large deposits. At this stage, it’s important not to make major financial changes—avoid opening new credit accounts, making big purchases, or changing jobs without consulting your lender.

Underwriting: The Deep Dive

Underwriting is the lender’s thorough review of your application, credit, employment history, and the property itself. An underwriter verifies that your income is stable, the DTI is acceptable, the credit profile meets program guidelines, and any red flags are explained. Underwriting may result in additional requests for documents, known as “conditions,” that you must satisfy before final approval. How quickly you respond to these requests often determines the speed of approval.

Appraisal and Inspection

Lenders require a home appraisal to confirm the property’s market value supports the loan amount. The appraiser evaluates comparable sales, property condition, and local market trends. Separately, buyers commonly arrange a home inspection to uncover structural or mechanical issues. If an appraisal comes in low, you may need to negotiate the price, provide a larger down payment, or choose a different lender. Significant inspection problems could also impact your willingness to proceed.

Final Approval and Closing Disclosure

Once underwriting conditions are cleared and the appraisal supports the loan, the lender issues a final approval. At least three days before closing, you’ll receive a Closing Disclosure that outlines the loan terms, monthly payments, interest rate, and closing costs. Review this document carefully and compare it with earlier estimates to ensure there are no unexpected fees or changes in terms.

Closing Day

On closing day you’ll sign the mortgage note, deed of trust or mortgage, and other legal documents. You’ll pay any remaining down payment and closing costs, either by certified check or wire transfer as directed by the closing agent. After documents are recorded with the local government and funds are transferred, the property title is officially yours. Keep copies of all paperwork and note the date your first mortgage payment is due.

After Closing: Servicing and Payments

After closing, your loan will be serviced by the lender or a servicing company that collects payments, manages escrow for taxes and insurance, and handles customer service. Establish automatic payments if possible and continue monitoring your escrow statements and interest rate situation. If your financial picture changes, contact your servicer—options like refinancing or forbearance may be available if needed.

Conclusion

While the mortgage approval process involves many steps and documents, each phase exists to protect both you and the lender. Preparation, clear communication, and prompt responses to lender requests are the best ways to keep the process smooth. With patience and organization, mortgage approval becomes a manageable path to achieving homeownership.