Overview of the Food Starch Market

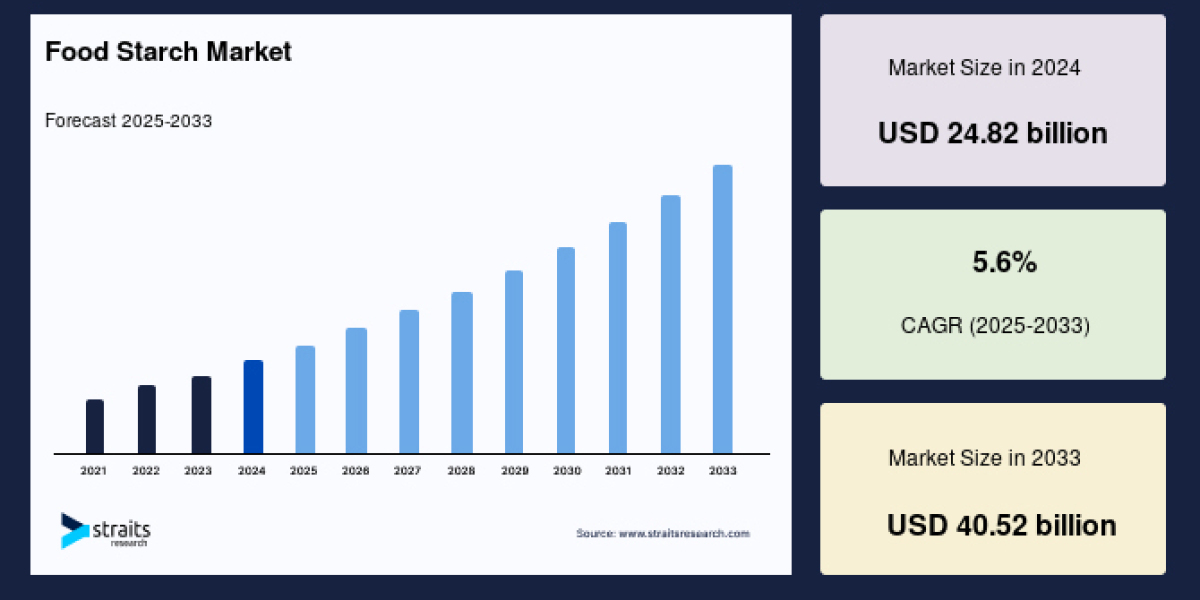

The global food starch market size was valued at USD 24.82 billion in 2024 . It is estimated to reach from USD 26.21 billion in 2025 to USD 40.53 billion by 2033, growing at a CAGR of 5.6% during the forecast period (2025–2033).

Key Market Drivers and Trends

The food and beverage sector's rapid innovation, improved supply chain logistics, increased affordability, growth in global trade, and higher consumer spending have strongly supported the expansion of the food starch market. Convenience food demand has surged as consumers increasingly seek ready-to-eat and cost-effective options, further boosting starch utilization. Moreover, the trend toward clean-label products that emphasize natural, non-GMO ingredients is reshaping the industry landscape. Major companies have responded by developing clean-label native starches, which perform comparably to chemically modified starches but cater to health-conscious consumers.

Regional Market Insights

Asia-Pacific accounts for the largest share of the global food starch market and is anticipated to witness a high CAGR of approximately 6.8% during the forecast period. This growth is fueled by rapid industrialization, strong government cooperation, and expansion strategies by food and beverage companies in countries like China, India, Japan, and Southeast Asian nations. The bakery and dairy segments, along with increasing demand for processed convenience foods, are major contributors to market growth in this region.

North America is a mature market and the highest revenue contributor. It is expected to grow at a more modest CAGR of around 4.2%. Early adoption of advanced food processing technologies, the introduction of non-GMO starch products, and continuous expansion of the food processing sector contribute to the market's performance. Europe also plays a significant role with substantial demand for bakery, dairy, and alcoholic beverage industries, along with a strong inclusion towards clean-label offerings.

Market Segmentation

By raw material, the maize (corn) segment holds the largest market share due to its high starch content and cost-effectiveness. Wheat starch and other starch types like pea and rice starch are gaining traction for their unique functional properties such as enhanced thickening ability, acid resistance, shear stability, and freeze-thaw stability. Pea starch, for instance, has become popular due to its high amylose content and superior functional characteristics compared to other starches.

In terms of type, the market includes native starch, modified starch, and sweeteners derived from starch such as glucose and high fructose corn syrup (HFCS). Modified starches—those treated enzymatically, chemically, or physically to enhance certain properties—play a vital role in improving the stability, texture, viscosity, and appearance of food products. Modified starches are widely used in bakery goods, sauces, and dairy products, and contribute significantly to reducing overall food production costs while improving quality.

End-User and Sales Channels

The food starch market is broadly categorized into business-to-business (B2B) and business-to-consumer (B2C) segments. The B2B segment dominates the market, driven by the food processing industry's large-scale use of starch as an additive for thickening, gelling, and stabilizing food products such as custards, gravies, soups, salad dressings, pasta, and noodles.

In the B2C segment, starch is available through specialty stores, supermarkets, and convenience stores, where consumers benefit from the ability to inspect products before purchase and avail attractive offers. The traditional retail channels continue to play a significant role in consumer access to starch and starch-based products.

Challenges and Opportunities

Despite its versatility, starch consumption faces potential challenges due to health concerns. Starch is a high-calorie ingredient that breaks down into glucose, influencing blood sugar levels and potentially contributing to weight gain. This aspect, combined with an increasing awareness of dietary health, necessitates innovation toward starch products that meet nutritional and clean-label demands.

Opportunities stem prominently from the clean-label movement, rising demand for natural and non-GMO starches, and expanding applications within convenience and functional foods. Manufacturers are also exploring new raw material sources like pea and rice starch to diversify supply and cater to niche consumer needs. Technological advances allowing for starch modification tailored to specific food applications hold promise for sustained market growth.

Conclusion

The global food starch market is positioned for robust expansion driven by evolving consumer preferences, the rise of convenience foods, and growing demand for clean-label, natural ingredients. Strong regional growth in Asia-Pacific coupled with technological advancements and product innovation in North America and Europe will shape the market landscape through 2033. With continuous adaptation to health trends and functional demands, the food starch industry is expected to remain an essential component of the global food supply chain with diverse application opportunities across food and beverage sectors.